Filing Deadlines for Canada Emergency Wage Subsidy (CEWS)

- Posted:

The federal government has provided recent updates regarding the Canada Emergency Wage Subsidy (“CEWS”) and other filing requirements for the wage subsidy programs. The Canada Revenue Agency (“CRA”) has also released new guidance on claiming home office expenses for the 2020 taxation year.

Introduced in April 2020, the CEWS initially provided a wage subsidy to qualifying employers who experienced a revenue loss during the 12-week period from March 2020 to July 2020 due to the COVID-19 pandemic. In July 2020, the CEWS was redesigned to provide an extension of the subsidy through to November 2020 and a revised framework that allowed for more employers to be eligible.

As of November 19, 2020, the CEWS has been extended to June 2021. The framework of the extension is similar to previous versions with qualifying employers being subsidized for a portion of eligible employees’ remuneration based on the extent of the revenue loss during the qualifying period.

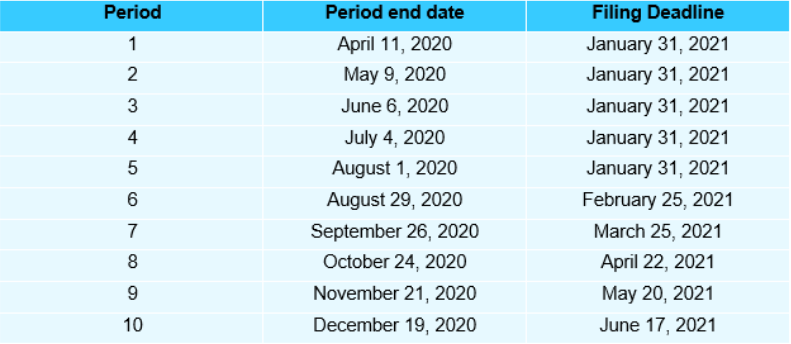

The deadline for CEWS applications is the later of January 31, 2021 or 180 days after the end of the qualifying period. The filing deadlines for each respective CEWS period are summarized as follows:

Requirement for the 10% Temporary Wage Subsidy Self-Identification Form

for Employers (Form PD27)

Another wage subsidy program that existed prior to the CEWS was the Temporary Wage Subsidy (“TWS”), which assisted eligible employers by allowing for a reduction in payroll withholding remittances to the CRA on remuneration paid during the period from March 18, 2020 to June 19, 2020.

The CRA requires all employers who qualified for both the TWS and the CEWS in the eligible period to file a Form PD27 for disclosure purposes. Even if the employer did not claim the TWS, they are still required to file the Form PD27 to ensure that they do not receive a discrepancy notice from the CRA. The form requires disclosure of employee payroll information including gross remuneration, income tax deductions, CPP contributions, EI premiums and TWS claimed in the eligible period.

Although there is no stated due date for Form PD27, it is advisable to submit the form before T4s are filed for 2020 to allow time for the CRA to process and update the employer’s payroll accounts.

Home Office Expenses and Form T2200S (Declaration of Conditions of Employment for Working at Home Due to COVID-19)

The CRA introduced Form T2200S, which is a simplified version of the standard Form T2200, specifically for individuals who worked from home in 2020 due to COVID-19. Due to the anticipation of potential administrative burden caused by issuing a large number of forms, the CRA has changed the claim process of the home office expenses by providing a temporary “flat rate” method and a “detailed method” for eligible individuals, which will only apply for the 2020 taxation year.

Under the flat rate method, individuals can claim a deduction at a flat rate of $2 each day they worked from home up to a maximum of $400, if they meet the following conditions:

- They worked from home in 2020 due to the COVID-19 pandemic, or was required by their employer to work from home;

- They worked more than 50% of the time from home for at least four consecutive weeks in 2020;

- They were required to pay at least some home office expenses (if reimbursed by employer, not all expenses were reimbursed); and

- They are not claiming any other employment deductions.

Neither Form T2200 or Form T2200S is required under the flat rate method given the above conditions having been met.

Alternatively, individuals can use the detailed method and claim the cost of home office expenses without a maximum limit (but not exceeding their employment income for the year), if they meet the following conditions:

- They worked from home in 2020 during the COVID-19 pandemic, or was required by their employer to work from home;

- They worked more than 50% of the time from home for at least four consecutive weeks in 2020;

- They were required to pay for the home office expenses (no reimbursement was received); and

- They received a signed Form T2200S or Form T2200 from their employer.

Form T2200S is required only when claiming office supplies and home office expenses under the detailed method. For individuals who are seeking to claim additional employment expenses (e.g. motor vehicle expenses), the standard Form T2200 is required.

Examples of eligible office supplies and home office expenses include:

- Paper, toner, ink cartridges, postage, etc.

- Utilities (i.e. electricity, heating, water), maintenance, and rent

- Property taxes and home insurance (for commission employees only)

- Mortgage interest or capital expenses are not eligible